ADVANCED ON PURPOSEAn educational blog with purposeful content. We welcome open and polite dialogue, and expect any comments you leave to be respectful. Thanks! Archives

May 2023

Categories

All

|

Back to Blog

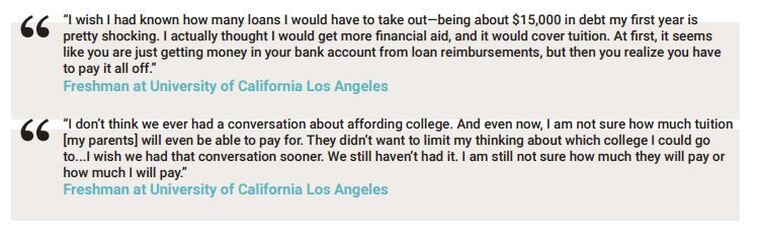

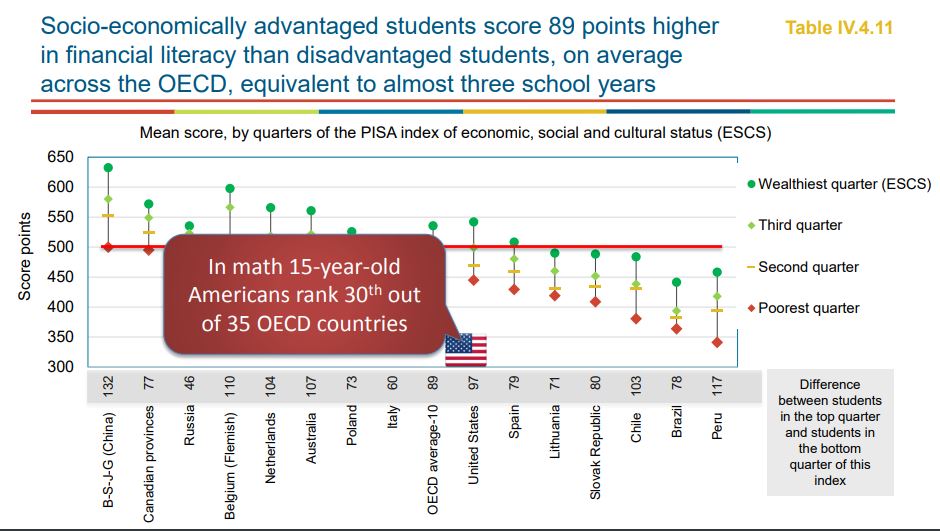

5 MIN READ This article picks up after the 4th article in a series on "Financial Aid, College Choice, and COVID-19"  In the last article in the series, Financial Aid, College Choice, and COVID-19, I spoke about the importance of supporting our students and families as they navigate the next steps in their college journeys by making sense of their financial aid options. In Supporting Students & Families through the Conundrum, I encourage college-bound students to “consider the power of savings and learn how to budget. You can make it work if you know what’s in front of you and take the time to thoughtfully plan it out.” This guidance should be given to students much earlier in this process, way before they apply to college. Comprehensive college access programs that work with first-generation and pell-eligible students often have a component in their curriculum that focuses on financial aid. Among the learning outcomes of such lessons, students will hear about budgeting and learn terms like “interest” and “credit” so that they can effectively manage their financial aid awards, like loans. In The Financial Aid Conundrum, I encourage us to take a step back and ask ourselves, “are our students truly equipped to tackle conversations and decisions around financial aid?” Because if the answer is no, then the next question should be, “what are we doing, or not doing, to help students understand basic financial concepts and empower them to make informed choices on their own?” As we learn from Treasury.gov, the financial literacy of our students in high school is lower than most countries. Furthermore, socio-economically disadvantaged students score lower in financial literacy, the equivalent of three school years.

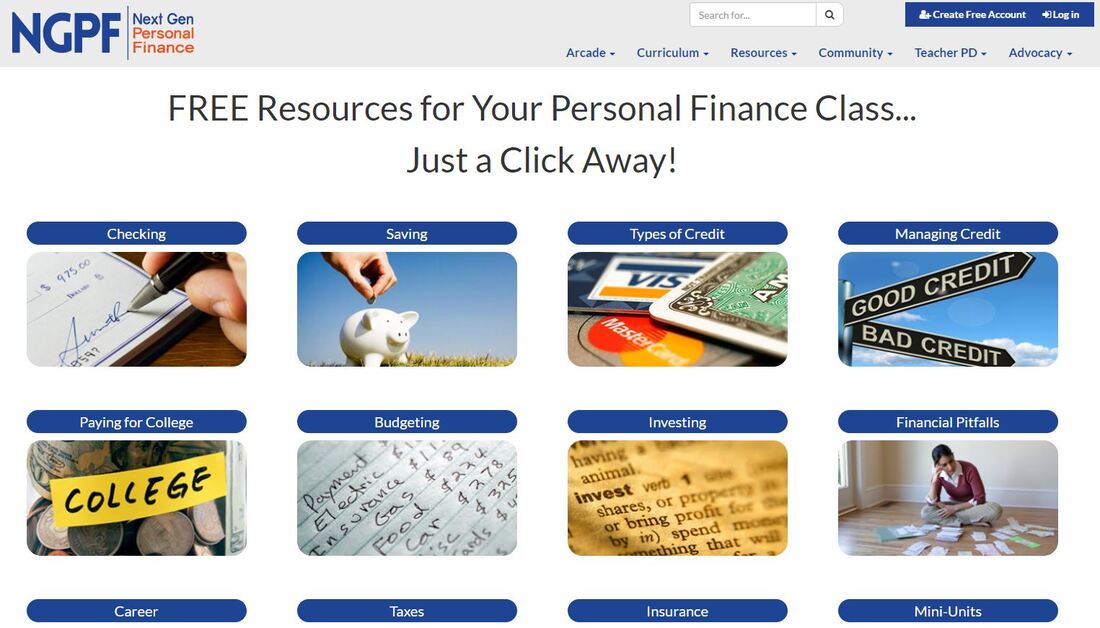

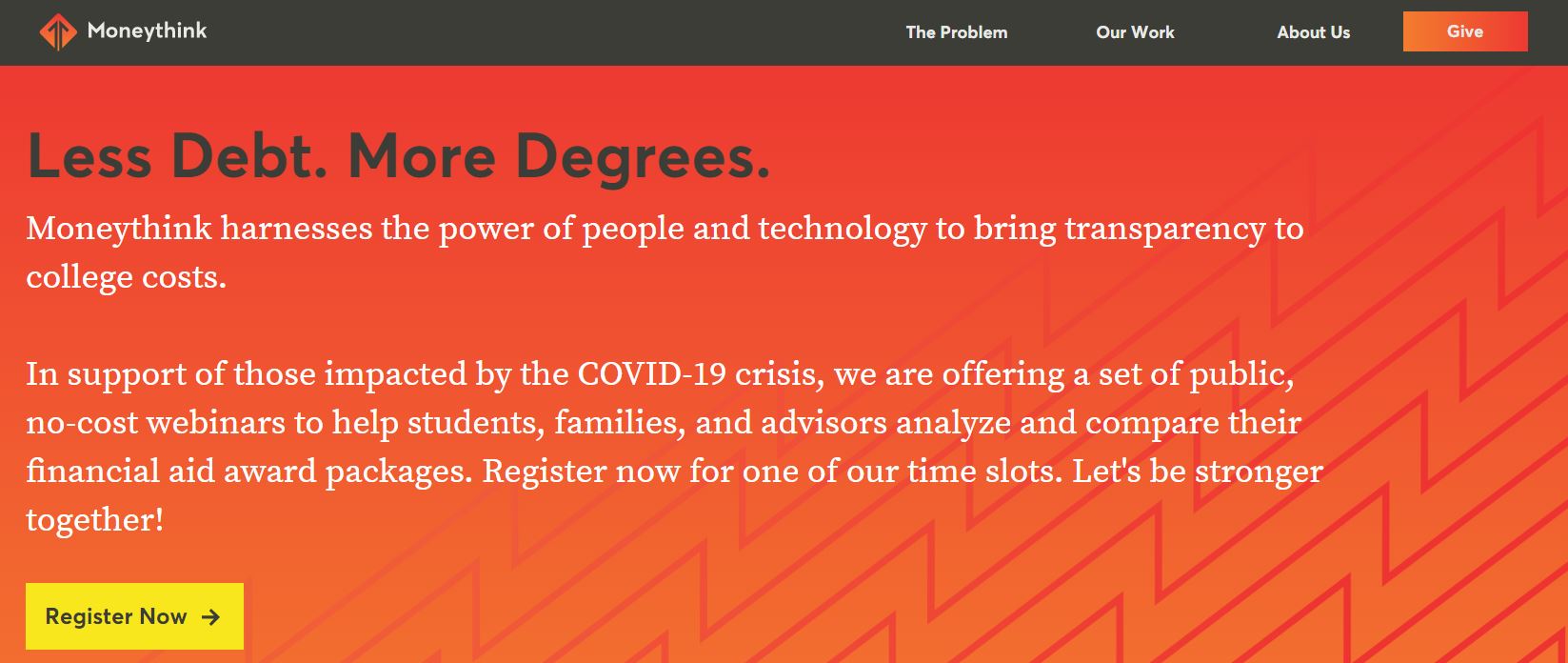

Here’s my attempt at making the relationships clearer:  How early should students build their financial literacy to prepare for college? ASAP, early, and often! I agree with Next Gen Personal Finance (NGPF) who decided in 2014 that it was critical to provide teachers with access to “timely and relevant curricular resources, providing effective professional development, and advocating to increase access to financial education.” NGPF’s mission is to revolutionize the teaching of personal finance in all schools in order to improve the financial lives of the next generation of Americans. As of 2019, NGPF's curriculum and professional development extends to 25,000 middle and high school teachers reaching more than 2 million students. This grassroots movement of personal finance educators has committed to Mission: 2030. That is, by 2030, ALL students will take a one semester personal finance course before graduating from high school. Personally and professionally, I think we can and should do even more than one semester of a personal finance course during students’ secondary education. It should start as early as elementary school, have scaffolding throughout middle school, and be grounded in real-life decisions during high school. NGPF has a suite of curriculum broken into various units such as Types of Credit, Managing Credit, Paying for College, Budgeting, and Financial Pitfalls.  Even when students are armed with the basic financial concepts they need to tackle financial aid, they will still need support. This is why I’ve worked with Moneythink since 2019 to support first-generation, pell-eligible students in navigating the financial aid process. Moneythink empowers students to invest in the future by building technology that clarifies college finances. In collaboration with the star-studded team at Moneythink, we hosted financial aid webinars in late April to support graduating high school seniors across the country. Check out the recording!  Moneythink is gearing up to release their new public-facing tool, DecidED, this fall! DecidED completely removes the guesswork out of college affordability for students and their families, as well as enables counselors and advisors in the space to have productive conversations with their students about the tradeoffs of college options. DecidED helps students and their families:

Check out how Moneythink is working to support students and advisors through COVID-19 and beyond. Follow and subscribe to Moneythink's email list to stay up to date. “Together, we can help our students not just survive but thrive. Not just complete, but succeed. Our students can achieve #lessdebtmoredegrees while we design a pathway towards an economically sustainable future for themselves and their families.” Want to learn more about financial literacy and financial aid issues?

Here are a few resources to help you build your knowledge and comfort-level with discussing these issues with colleagues, students, and families.

2 Comments

Back to Blog

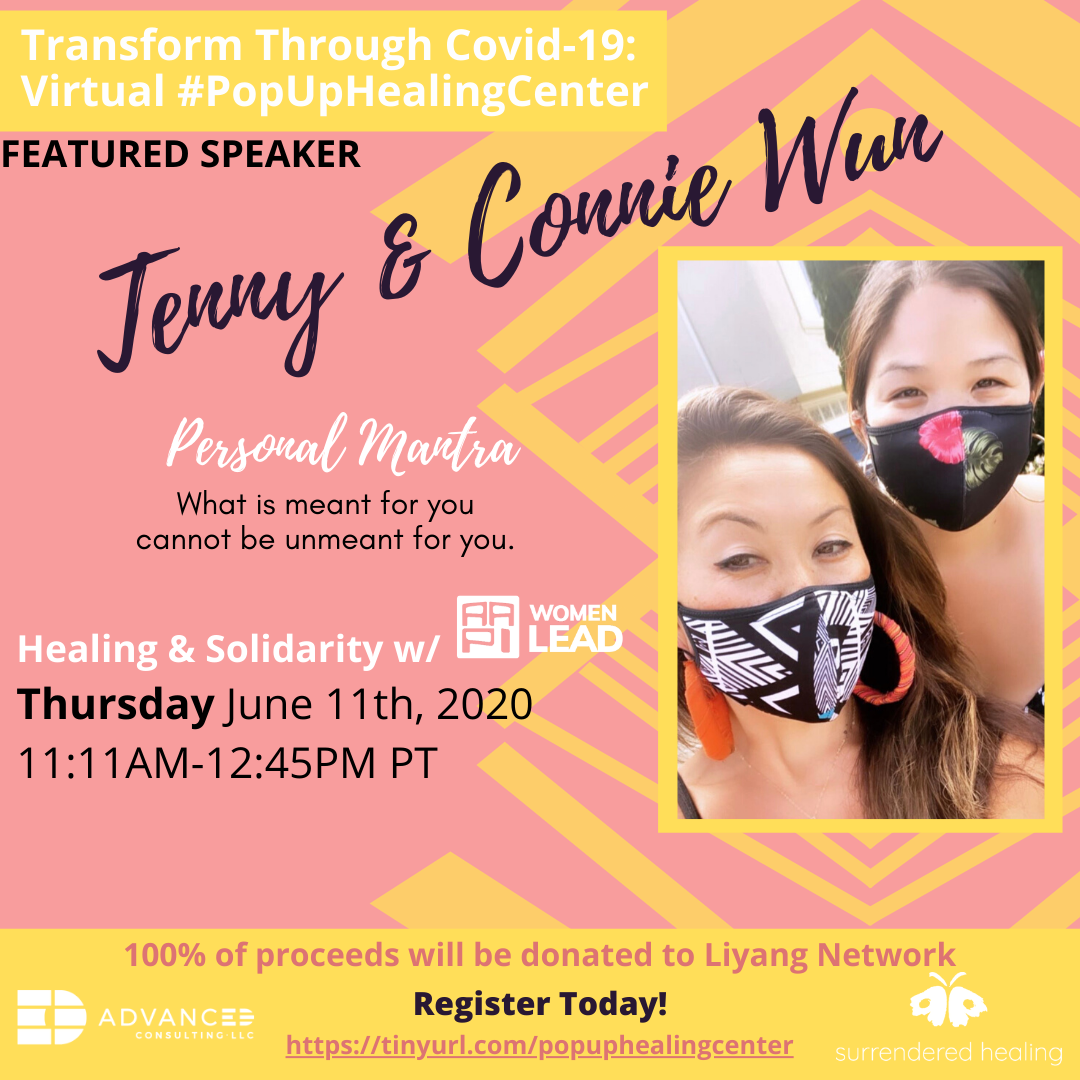

Heal at 11:11, Heal for Life5/27/2020 3 MIN READ  FOR IMMEDIATE RELEASE CONTACT: Meredith Curry, Owner & Principal Consultant of AdvancED Consulting, LLC mer @ advancedconsulting.org Over 20 Healers of Color From Across the Country Deliver Free Healing When It’s Needed Most Heal in Solidarity: Starting on Saturday, June 6, 2020, AdvancED Consulting, LLC and Surrendered Healing, solo entrepreneur women of color from the Bay Area, will offer a Virtual #PopUpHealingCenter for free for seven afternoons straight. What do we mean by healing? Well, does your heart hurt? Or your head? Does your bank hurt? Do any relationships hurt? Then you can use some healing! And this event has over 20 people ready to support your healing through movement, creativity, and mental enhancement. "11 is a 'master number' which signifies intuition, insight, and enlightenment. When paired together, 11 11 is a clear message from the universe to become conscious and aware" (truththeory.com). This is why every day from Saturday, June 6 through Friday, June 12, “Transform Through Covid-19” will start at 11:11 am with a grounding meditation to start the day led by Surrendered Healing Founder and Spiritual Healer, Adelina Tancioco. Next will be three 20-minute sessions from healers of color from across the country representing the Bay Area, Los Angeles, Fort Washington, and the Bronx. Each day will end at 12:45 pm with 15 minutes of rhythmic movement led by Meredith Curry, Owner of AdvancED Consulting, LLC, and music by Shanta Franco-Clausen, a.k.a. DJ Shugga Shay. “Our work is sacred and so are we,” shares Tovi Scruggs-Hussein, Educational Leader & Healer with Tici’ess, Inc. in Oakland, CA who will lead a session called “$tackin' for Spirit: Keeping Your Money Conscious, Connected , and Courageous.” We invite you to be a part of this virtual healing community by registering for “Transform Through Covid-19” and enjoying one day, or everyday of the week-long event. This is for you if:

To learn more and register, go to www.advancedconsulting.org/pop-up-healing-center. Read the profiles of the event speakers and explore nearly two dozen sessions. Fawad Akbar, Owner of Body Evolution in Newark, CA believes, “Two things define you. Your patience when you have nothing, your attitude when you have everything,” and he will share this with us in practice in his session “Full Body Workout with Body Evolution.” “Transform Through Covid-19” is proud to partner with AAPI Women Lead founders Dr. Connie Wun and Jenny Wun who will lead a day of Healing & Solidarity. “What is meant for you cannot be unmeant for you,” shares Jenny who will lead a session with her sister called “Healing & Solidarity.” The event also promotes a fundraiser to support the Liyang Network during COVID-19. 100% of contributions will go to services, resources, and supplies for the Lumad, the indigenous people of Mindanao, Philippines. “Lumad” means “native of the land” in Cebuano. In celebration of the Lumad and all Filipino cultures, there are healers offering sessions like "BAKS NAMAN! Self Care through Boxing;" "Dalawang Buslo, Two Baskets: Integrating Stress & Joy in the Present Moment;" and "Hilot Through Story." For more information about Transform Through Covid-19: A Virtual #PopUpHealingCenter with 21 Healers of Color or to arrange an interview with the co-hosts Meredith Curry and Adelina Tancioco, please contact Meredith directly at [email protected]. ### Meredith “Mer” Curry is the Owner and Principal Consultant of AdvancED Consulting, LLC. Mer’s mission is to empower businesses striving to solve the world’s most complex issues through thought-partnership, education, and operational leadership. She also seeks to uplift organizations run by and/or actively promoting the betterment of hxstorically disadvantaged groups like minorities and womxn. Mer works with entrepreneurs, nonprofit and education organizations to increase capacity organization-wide. She works with their leaders and professionals to enhance fund development, board management, programming, data analysis, Salesforce, and general operations strategies and processes. For more information see www.advancedconsulting.org or follow Mer on LinkedIn and Facebook.

Back to Blog

7 MIN READ This article is the 4th in a series on "Financial Aid, College Choice, and COVID-19" The time is now to support our students and families through this financial aid conundrum and ensure they’re making the best choices for their futures. In the first article in this series, Financial Aid, College Choice, and COVID-19, I talk about the importance of all of us working together right now because as adults, as students, as human beings, if we’re going to get through COVID-19, it will be together. In the second article, I talk about how we face a Financial Aid Conundrum that is persistent, systemic, fraught with pitfalls ready to take advantage of families, and overbearingly complex to tackle. I talk about this now because this issue is facing our students right now as they prepare to choose what college they will go to by the College Decision Day deadline of May 1 for many California public and independent four-year institutions. When all is said and done, though, we must keep in mind the Power of Student Resilience and Choice. That's why in this fourth article, I want to address the students so that they can recognize this power. I also address all adult allies so that we can support students in embracing said power. Students, you can do this!

“Take an entrepreneurial approach and focus on sectors that are growing. Even if these areas don’t align with what you imagined you’d be doing after graduation, cultivate a flexible and open mindset - this will be essential for students in a COVID-19 economy. Build your energy as if you’re preparing for a marathon not a sprint. In the weeks and months ahead, be patient with and kind to yourself and develop support systems. Consider the possibilities that may emerge (in time) for us as a society, when many communities and sectors begin to focus on rebuilding.” Allies, we can help them!Colleague Lara Fox, Senior Advisor at the Marin Community Foundation who served prior to that as the Founding Executive Director of uAspire Bay Area, has this advice for us adult allies and educators: "It's crucial that counselors both stay in regular contact with 12th graders and ensure that students know they can appeal their financial aid offers if family circumstances have recently changed. It's also essential that colleges prepare to respond to a likely increase in appeals, given that 22 million Americans have filed for unemployment in the past four weeks alone.” I know the financial side of college can be daunting and overwhelming and I just hope families and educators will work together to ensure our students make the most of their options. Allies, let’s help our students now as much as we can, while also thinking strategically about how to support future cohorts through this. If you are a college advisor, counselor, or educator, consider teaching your students financial literacy, especially now, but also much earlier in students’ high school careers. Next Gen Personal Finance (NGPF) has a curriculum called “Paying for College.” Here’s a snippet of what you can teach your students using NGPF's lessons:

Colleges, please consider your students!To colleges and university financial aid officers and advocates, thank you for keeping students at the center. Please continue to do so. Our colleges will also need to support families, now more than ever, so that they can advocate for the best deals that will lead to less debt and more degrees. The Community College League of California Financial Aid Office Operations Taskforce released the report “Increasing Student Access, Success and Equity: California Community College Student Focused Financial Aid Policies February 2020” with the following guidance. Though written for community colleges, they bear consideration for all higher education institutions.

And finally, some Best Practices they offer for higher ed:

Thank you for sticking through this series on Financial Aid, College Choice, and COVID-19! Good luck to the #ClassOf2020 and all non-traditional students who are preparing their choice for College Decision Day this year! To learn more about Moneythink, go to moneythink.org/. To learn more about Next Gen Personal Finance, go to www.ngpf.org/.

Back to Blog

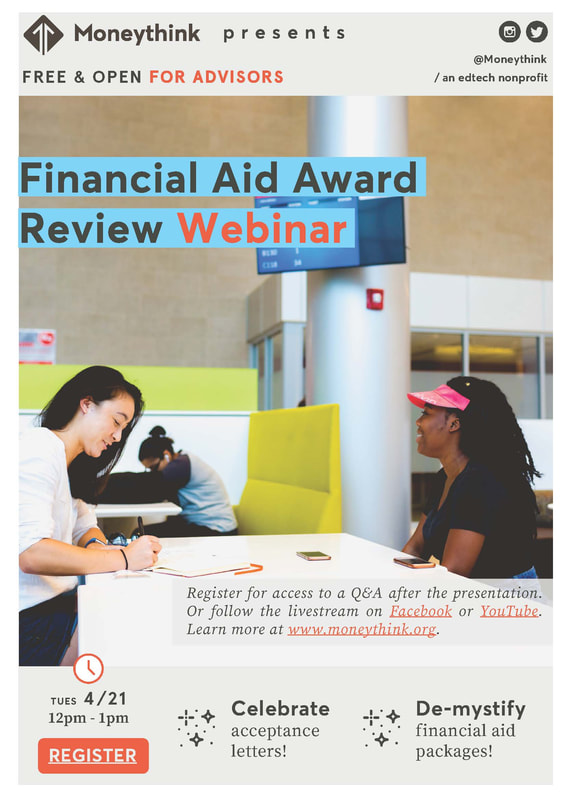

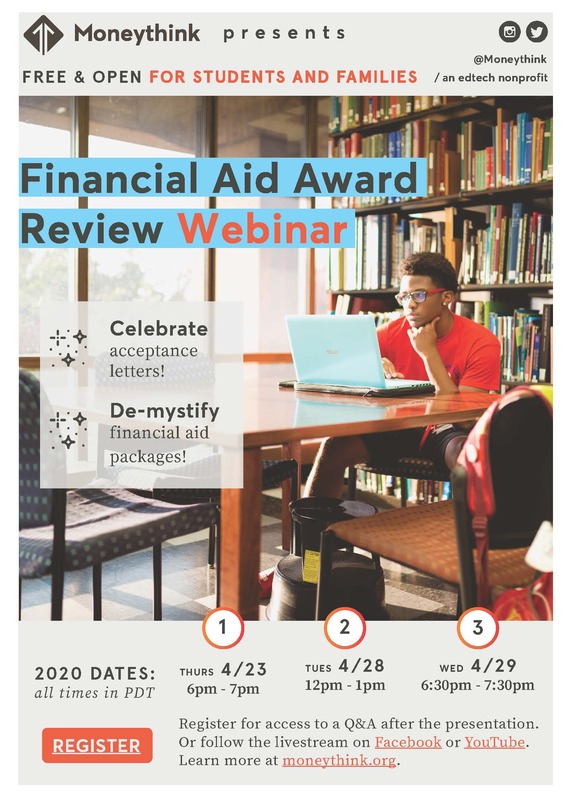

5 MIN READ  This article is the 3rd in a series on "Financial Aid, College Choice, and COVID-19" COVID-19 will impact college decisions this year. National College Decision Day is historically on May 1. There are petitions to push back Decision Day to June 1 if not later. From the New York Times (March 15), the Washington Post (March 20), NPR (March 22), and CNBC (March 27), we hear that the college decision experience is impacting students and colleges alike with the cancelations of college visits and Admit Days nationally. Affordability is an even bigger concern today than it was prior to COVID-19 with less than ¼ of students having a high level of confidence in their ability to afford college now (Carnegie Darlet). Families’ investments are getting hit and both students and parents are less sure about how their jobs and paychecks can contribute to college expenses this fall. Students’ perceptions of where they want to go are changing. They’re considering less-expensive and local public schools over private universities far from their families, and 70% are thinking of staying within 3 hours (or 180 miles) from home (The Princeton Review). The American Council on Education has predicted a 15% drop in enrollment nationwide (and 25% international), and many institutions are preparing for the possibility of having to continue remote classes or delaying the start of the fall semester to reopen campuses (NY Times). How can you help your students and families navigate this crucial time in their lives, so that they can still take advantage of opportunities that are best for the student?  Step #1: Choose a tool to analyze your student’s award letters. In the first article in this series, "Financial Aid, College Choice, and COVID-19," I introduce you to partner Moneythink. I recommend Moneythink’s coaching tool that you can download to Excel. It pre-populates information from most colleges that have public direct and indirect costs data and all you need to do is override it with any actuals your colleges provide in their letters! Why does Moneythink pre-populate information when other tools don’t? Because this highlights one of the main issues with financial aid award letters: they often have incomplete or misleading information. This could be in the form of information that is literally missing, like no reference to personal expenses or transportation, or no specific mention of PLUS loans though they are included in the package. Step #2: Have your financial aid advocates at the ready. Connect with your high school guidance counselor or college advisor. If you work with a college access organization you can reach out to your advisors and let them know you’re looking for help. Take advantage of free webinars like Moneythink’s Financial Aid Award Compare Webinars scheduled on April 21 for Advisors and April 23, 28, and 29 for Students & Families.

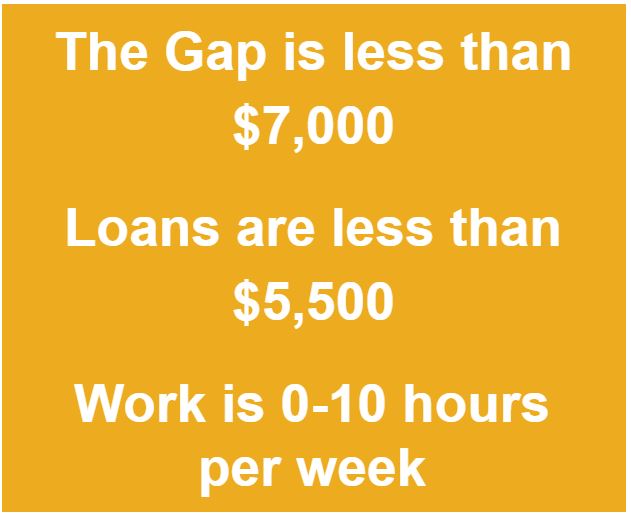

Step #3: Collect and compare those awards! You don’t have to review all of your award letters at once. In fact, you should review them as you get them so that you can advocate as soon as possible when you need to! The sooner that you appeal when it is the right move, the better. As you get the awards, compare them. Did College B offer you a better package (comparing gift aid to direct costs) than your first choice, College A? Get your appeal package together and let College A know about College B’s offer. See if they’ll budge! For more tips on appeals, check out SwiftStudent which helps you write your financial aid appeal letters for free.  Step 4: Advocate! Advocate! Advocate! Students are unaware that funding sources can vary year to year. Families often don’t know to ask if the institutional grant they were awarded is renewable for future years. Sometimes they don’t know to ask their scholarships where their money is going, and this matters because some colleges will take scholarship money reported to them and we’ll see a case of financial aid displacement. This means the colleges reduce the amount of gift aid like grants by the size of the scholarship. Advocate for the best awards by ensuring they’re basing it off the most up-to-date information, appealing if you have a qualified circumstance, and applying to as many scholarships as possible. Do what you can to fill whatever gap is standing in the way of you and your college. But be sure you’re thinking about more than just this year. Ask all the questions you need to so that you understand what financial aid could look like for your 2nd year and future years. Colleges often offer very appealing first-year packages but they start to look different in the 2nd year. That’s why groups like AAUW San Jose have a scholarship just for college juniors and seniors! Step 5: Take out only the necessary loans and work study. Loans can be a very important, necessary, and positive investment in your future. Taking out more loans than you need to, however, can be costly. There is also an opportunity cost when you work more hours than will allow you to focus on your studies. The guidance from Moneythink for a college to be affordable is:

So be sure to pay attention to affordability, but don’t lose sight of other things that matter to you about the campus. Factors like the diversity, the culture, whether they offer the major or program you like, on- and off-campus activities, and whether or not you can really “see” yourself learning and growing there (whether you stick to the original major or not). Lastly, whichever college you decide to pursue, if you believe the Enrollment Deposit is a barrier for you and your family, advocate for yourself. The National Association for College Admission Counseling (NACAC) has released a new form for counselors, college access advisors, students and their families: Enrollment Deposit Fee Waiver Form. This form allows a student to request that their enrollment fee be waived due to financial circumstances. Enrollment deposits can be as low as $200 to as high as $600 (or even higher!), which can be a barrier, especially for low-income students. While everyone can use this form, each college can manage their own policies, choosing whether or not they will accept this form. I believe that there are student-focused financial aid officers out there waiting to support you through these challenges, so if you’re ready to make your final decision but you can't come up with the deposit money for your preferred college, submit the Enrollment Deposit Fee Waiver Form ASAP. I highly recommend that you do this before the deadline. Not sure when the deadline is? Check NACAC’s College Admission Status Update page with over 1,000 college updates so far. In the next article, I want to talk about Supporting Students and Families Through the Conundrum.

Back to Blog

3 MIN READ

"Thank you to my mother Helena Curry who instilled in me a strong work ethic, grit, and drive and paved the way by showing me what it means to be a true grassroots community leader and social justice advocate." Acknowledgments I thank the partners of AdvancED Consulting, the Santa Clara County Commission on the Status of Women, the Santa Clara County Office of Women’s Policy, and the many local and statewide college, career, nonprofit, civic, and social justice advocates who shared contacts, made introductions, and dedicated time to provide all of the wonderful information listed in this guide. A big shout out goes to Amparo Diaz, Annie Do, and Michael Nuñez, all AdvancED Consulting partners, who supported the design and organization of content in this guide. Shout out to Kyra Young who designed all of the affirmation stickers and other AdvancED graphics you see throughout this guide and the AdvancED website and social media. Thank you to my partner (in life and career) Michael who supports me in all things and empowers me to be of service however I can as my authentic self. Thank you to my mother Helena Curry who instilled in me a strong work ethic, grit, and drive and paved the way by showing me what it means to be a true grassroots community leader and social justice advocate. Thank you to my cousins Janella Parucha, Justin Parucha, Melinda Parucha, and Evita Dupitas who inspire me to be myself and love myself. Thank you to my aunt Hedy Parucha and uncle Ben Parucha for their constant love and support. Thank you to mentors like Dwayne, Claudia, Coleetta, Sr. Susan, Gloria, Allison, Tessa, MB, Trisha, Dr. London, Masai, Elroy, Eric, Kevin and so many more for your wisdom, selfless coaching, and well-intentioned feedback. Thank you to great friends and colleagues like Lara, Gina, Erin, Meo, Serei, SJ, Alerie, Rod, Kadar, Matt, Meghann, Andrea, and Anthony for the strength you give me, each other, and the world, with all of your unique gifts and strengths.

Back to Blog

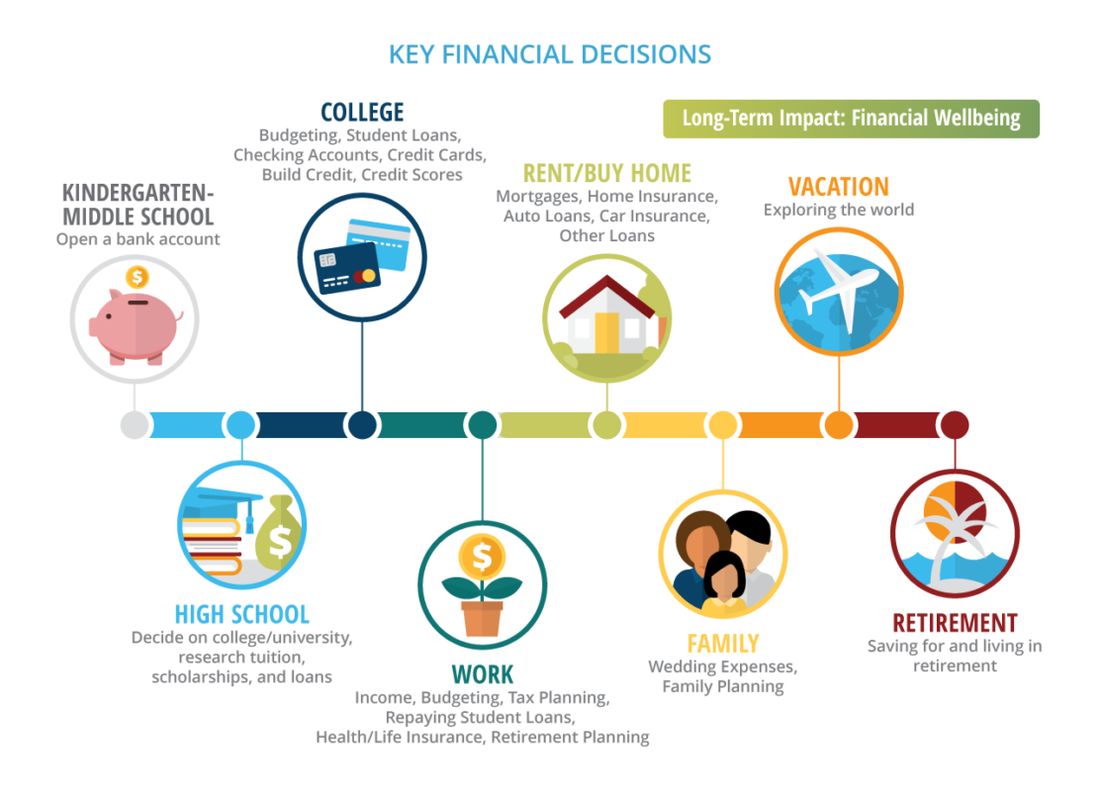

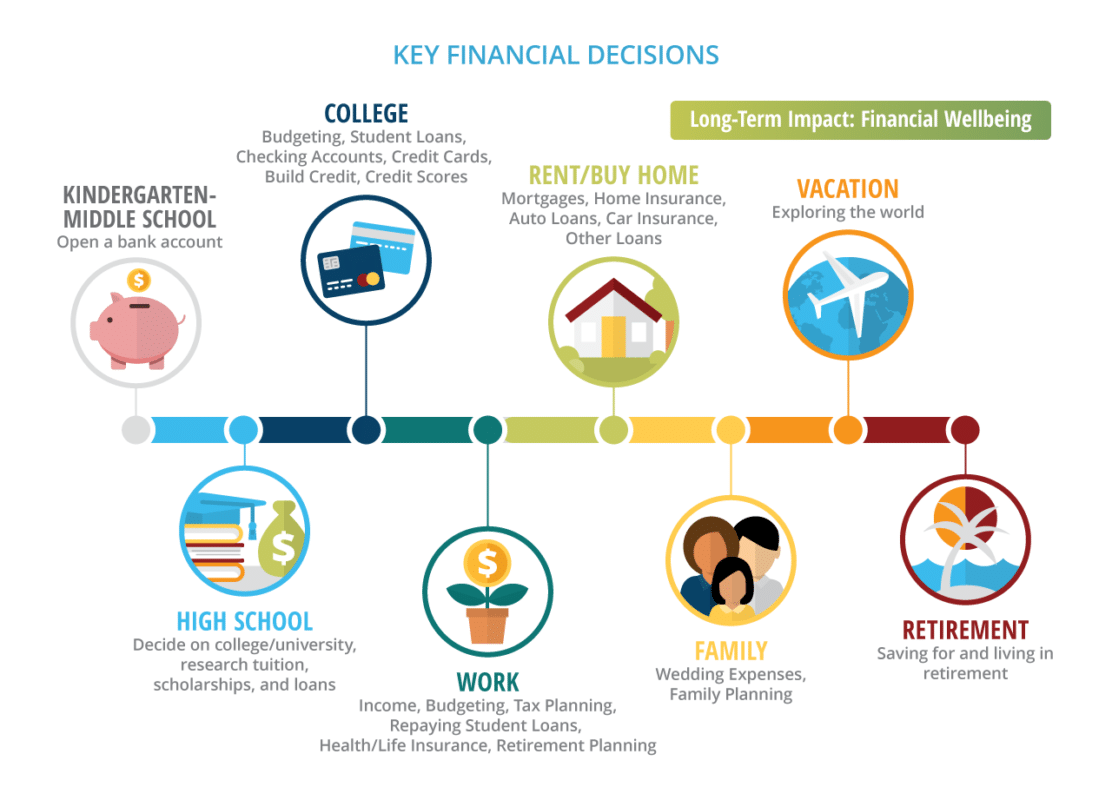

The Financial Aid Conundrum4/15/2020 13 MIN READ  This article is the 2nd (and longest!) in a series on "Financial Aid, College Choice, and COVID-19" There are a lot of key financial decisions that we need to make as humans in this country. As you’ll see from the image below, they really start in high school with college-related decisions. When I think of this time in our high school seniors’ (and non-traditional students’) lives and put myself in their shoes, the two questions that come up for me are: 1. Am I going to college this Fall or Spring, and 2. If I am going to college, where?  There is actually a third question, since there is a financial component to both questions. That question is 3. Depending on where I go to college, how much will I have to pay to go there? and this question is what I refer to as the Financial Aid Conundrum. It’s a conundrum because, firstly, I really enjoy that word and have few opportunities to use it. Secondly, because the synonyms for conundrum are in line with what students, families and educators face when it comes to financial aid, synonyms like “enigma,” “mystery,” “brain-teaser,” and “problem.” In the first article in this series, "Financial Aid, College Choice, and COVID-19," I talk about the power of networking and how I learned about Next Gen Personal Finance (NGPF) and their podcast "Tim Talks To..." In one podcast, what Melissa shares with Tim Ranzetta gets at the heart of what college-bound high school seniors are struggling with RIGHT NOW, and with 3.7M high school seniors expected to graduate from high school this 2019-20 school year according to the National Center for Education Statistics, it will require a huge, coordinated, all-hands-on-deck approach. Let’s all work together, utilizing all the expertise and tools in our toolbelts to support all these seniors through not just high school graduation, but also through important decisions that will impact their futures. Because many of these decisions are FINANCIAL. Here is the financial conundrum broken down into three (3) issues. Grab a seat and get comfy.  Issue #1 This issue affects all students, but disproportionately for low-income students of color. Moneythink has done a ton of research on this issue, and there’s plenty of great information out there speaking to the issues of college persistence and student debt. Here are three facts we want you to know:

What does this all mean? That despite our best efforts to get students to college, especially first-generation students, they are ending up with too much debt and the lack of clarity about financial aid is largely to blame. Debt is a huge persisting problem since so few colleges are considered affordable to students struggling the most to pay, and to make things worse, students end up with debt whether they get their certificate or degree or not. If students are choosing (though, we argue, without a clear understanding) to go to unaffordable colleges, they are more likely to drop out because of financial reasons. If they knew they were doing this, would they willingly take out thousands of dollars in loans without the promise of an actual degree to make it worth their investment? Most of us education advocates, advisors, and counselors would argue of course not. So the question is, how do we get students to be more informed and empowered owners of their college choices? Let’s first look at how students understand this choice, and who helps them to understand.

In Moneythink’s College Success Report which they published in 2016, student interviews revealed two driving factors of students’ financial vulnerability:

Students are also not having open and honest conversations with their parents about how they will be paying for college, and not because they don’t want to, sometimes because they just don’t know how to. While as allies and advisors, we might want to be in these conversations with each and every student to guide and support them, it’s just not possible given our bandwidth. I recommend resources like Moneythink and CaliforniaColleges.edu that offer talking points for students on how to talk to their families about money. Tools to bring clarity to families Even if a student has open and honest dialogue with their families about money, the process of reviewing and analyzing financial aid awards is still very convoluted, and unnecessarily so. The financial aid award is the only document that will tell families how much college will cost. Unfortunately, despite the availability of an aid template provided by the Department of Education to both simplify and clarify financial aid, colleges have their discretion to use whatever manner of jargon and incomplete information makes sense for their cultures, which leads to misleading information that often prevents families from using them effectively to make informed, intentional decisions. According to a report by New America & uAspire:

The Department of Education offers comparison tips on its website, and the National Association of Student Financial Aid Administrators (NASFAA) offers a worksheet, which students and families can print out, to help keep information about different colleges organized. Community capacity The research shows us that our community doesn’t have the capacity to provide quality college advising and counseling when it comes to financial aid, even with the best intentions at play:

Despite the best efforts of our colleagues in the field, financial aid is incredibly confusing, it changes on the regular, information from the powers that be don’t regularly or clearly trickle down to the people on the ground that need to disseminate the information to students, and training is not readily available to solve for the lack in knowledge and experience. The Powers That Be The Federal Student Aid office has recommended that colleges include the cost of attendance in aid letters and clearly distinguish between grants and scholarships, which don’t need to be repaid, and loans, which do. (Federal Student Aid) The Powers That Be, or the colleges that are designing and distributing their financial aid award letters, are recognizing the problem but are operating on their own timelines and priorities to solve this issue for students. Now that we’ve fully discussed why the Financial Aid Conundrum is such an issue not just for all students, but especially for low-income, first gen students, let’s look at the remaining issues because yes, there are still more.  Issue #2 College decisions don’t focus enough on the financial considerations and implications. College decisions are about both WHERE a student is going to spend the next 1-6 years of their next academic and career journey, and HOW MUCH they are going to pay over time as an investment in their future. The process of evaluating financial aid awards requires multiple complex steps. Every single one of these steps requires a level of maturity and mathematical savvy, and for the right information to be in students’ hands all at once. In Moneythink’s interviews spanning thousands of students, many students shared that they were left unassisted and confused during the process. In many cases, students were not adequately prepared for college. In some cases, students received the help that they needed to be accepted into the school of their choice, thanks to the support of well-intentioned family, engaged college counselors, and available college access programs. Unfortunately, they were often expected to figure out the rest once they got to college, especially when it came to the finances.

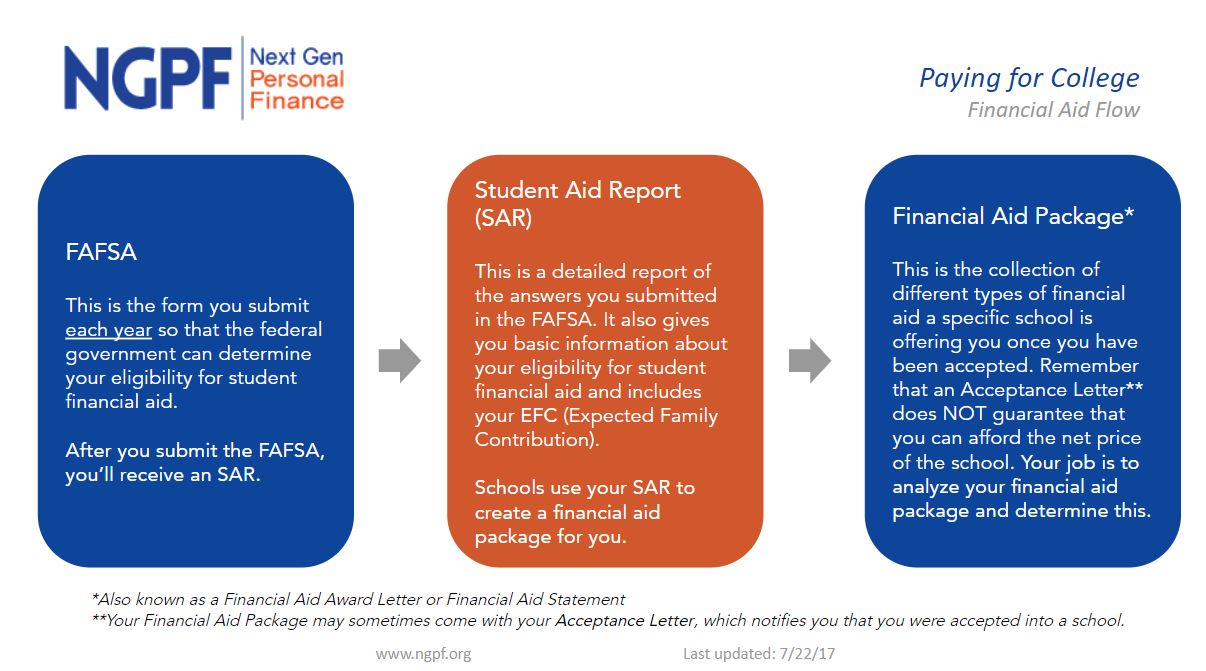

Organizations like ScholarMatch, Students Rising Above, Richmond Promise, the Early Academic Outreach Program (EAOP), Destination College Advising Corps, and more, serve students during the crucial transactional steps of their senior year and will walk students step-by-step through the financial aid application process. Once students complete their FAFSA, they will receive a Student Aid Report (SAR) and that will offer an Expected Family Contribution (EFC). A student EFC of zero (0) is the lowest possible value, and it means that the family has no ability to contribute to the student’s education. The highest EFC is $99,999.  After a student submits their FAFSA, they may be asked for more information. This is called Verification. The SAR will note if the student has been selected for verification, or the college may contact the student directly. “Verification is the process your school uses to confirm that the data reported on your FAFSA form is accurate. If you’re selected for verification, your school will request additional documentation that supports the information you reported.” (Federal Student Aid) Once you’ve made it through verification, you should have a final award letter, as opposed to an award estimate. You will need to review this award letter so that you understand:

Earlier I shared that there are tools out there to help figure out the financial aid award review process. The problem, however, isn’t the lack of tools to help clarify and make sense of award letters. There are tools out there like the FinAid Letter Comparison Tool (with an advanced version available), BigFuture’s award tool, or CaliforniaColleges.edu’s use of the CollegeOPTIONS’ Financial Aid Award Comparison Tool. The real problem is that, while tools exist to compare financial aid awards for multiple colleges, these tools often require:

There is no tool out there that supports students and families in better understanding their financial aid award letters that does not also require them to manually enter that information into some document. This is fraught with user error and is a barrier to entry in multiple ways (lack of technical skills, variance in how award letters name and describe aid, incomplete awards, etc.). This is why I’m excited for Moneythink’s award compare tool coming out in October 2020 that will let you take snapshots of your awards for a super-fast analysis! Want to learn more about it? Click here to get on Moneythink’s listserve!  Issue #3: Students often don’t realize just how much power they have in their college choice.

Despite all this challenge and calamity, there is still hope! Students DO have the power of their choice. Students DO have the time and opportunity to look at all the information available and make an informed, intentional decision about where they’re going to go this Fall or Spring. Students CAN and SHOULD resolve to make choices in their best interest that help meet goals they have designed for themselves. And as the parents, advisors, counselors, educators, coaches, guardians, and adult allies in their lives, we CAN and SHOULD resolve to support them however we can to make the best, most affordable decision possible. In this next article, I want to talk about how students can do this. It’s time to talk about The Power of Student Resilience and Choice because you DO have choices as a student. Students: The power to choose IS ALL YOURS.

Back to Blog

4 MIN READ  This article is the 1st in a series on "Financial Aid, College Choice, and COVID-19." The power of “friendraising” has never been more real than in a recent introduction by a local education advocate which led to a podcast interview. I’m here to tell a story that starts with education colleagues making connections, and ends with the power of student resilience and choice. In this series, I start first with the alchemy of networking and friendraising because as adults, as students, as human beings, if we’re going to get through COVID-19, it will be together. Thus, I start with a Tale of Six Colleagues. As I continue the series, I wish for high school seniors, transfer students, parents, educators, and their allies to know that when it comes to financial aid and college choice, we face a Financial Aid Conundrum that is persistent, systemic, fraught with pitfalls ready to take advantage of families, and overbearingly complex to tackle. I then want to take a hopeful stance by talking about the Power of Student Resilience and Choice. I want students, and all of your allies, to understand that in your hands is the power to choose the best fit college for you based on what’s both affordable and a strong match. Lastly, I will close with how we can all support students through this, whether you are a student or an ally. Supporting Students & Families through the Conundrum means securing the futures of our communities, our cities, our counties, our states, our nation, and our world. Again, we are all in this together. Let’s begin with why networking matters. If you already know why networking matters, you can skip ahead to the meat of this series with the Financial Aid Conundrum.  A Tale of Six Colleagues It started with me (Colleague #1) reaching out to Todd Hicks (Colleague #2), Director of University Access and Success at Cristo Rey San Jose. Thanks to my career development and college access related projects with partners Management Leadership for Tomorrow and Moneythink, and general volunteer work across Santa Clara County, I had more than one reason to sit down with this local educator. Cristo Rey San Jose is a member of the Cristo Rey Network which has 37 schools across 24 states. At the time I was in conversations with Todd about how to best support first gen students, I was in the planning stages of financial aid award review webinars with CEO Joshua Lachs (Colleague #3) of Moneythink. Moneythink empowers students to invest in the future by building technology that clarifies college finances. Thanks to Joshua’s leadership and his star-studded team at Moneythink, we were planning to host financial aid webinars in late April to support graduating high school seniors across the country through a crucial date that is fast-approaching: College Decision Day.  One conversation in Todd's well-organized office turned into multiple emails, text, and phone calls excitedly charged around the topics of educational equity, access, and student success. In our most recent insightful encounter, Todd introduced me to Christian Sherrill (Colleague #4), Director of Business Development and Advocacy at Next Gen Personal Finance (NGPF). Appreciating every opportunity to meet a Teach for America Corps Member continuing to do great work for underserved populations, I eagerly scheduled our chat. Reaching more than 2 million students nationally by serving 25,000 middle and high school teachers, I was thrilled to learn more about their free personal finance curriculum and professional development offerings. Christian shared that NGPF’s mission “is to revolutionize the teaching of personal finance in all schools and to improve the financial lives of the next generation of Americans.” This wonderful chat with Christian in March turned into an introduction to NGPF Co-Founder Tim Ranzetta (Colleague #5) who also runs a “Tim Talks To…” Podcast. I was thrilled to listen to some of the episodes, such as Demetria Gallegos of WSJ on 9 Myths About Credit Scores from January 10, 2020 and Melissa Santoyo on the importance of financial education for first-gen students from November 29, 2019. Listening to Melissa’s podcast got me super excited for my chat with Tim because something she said really struck me: "I think that we need to prioritize teaching kids how to read financial documents, how to interpret them, how to walk into a college application process feeling at least a little bit more confident about the things we're in control of... when it came to the financial documents, I felt rather helpless. Because, you know something that was supposed to be in my control, something that I should have been able to fill out and then move on with my day, that wasn't the case. It carried this immense panic, and stress and anxiety and worry, further exacerbating the general horrible feeling of the college application process. So something needs to be done, and it needs to be done earlier on." When Tim asked me how I learned about Moneythink, I was pleased to share that it was through a mutual connection, Lara Fox (Colleague #6), Senior Advisor at the Marin Community Foundation who served prior to that as the Founding Executive Director of uAspire Bay Area. Lara not only introduced me to Moneythink, she also mentored me through my first year as a consultant. With connections made, Tim interviewed me for his podcast. What I shared then is a snippet of what you'll read in this series.

Now we’ve come full circle! On to the challenge at hand...the Financial Aid Conundrum. |

RSS Feed

RSS Feed

{kind=link}

Photo from CityofStPete